The truth behind smart driving programs and what they track

As an Amazon Associate, some links pay us a commission at no extra cost to you. Keeps this website free. Thank you.

I'll break down exactly what insurers collect — and how they use that data.

r/GEICO via Reddit.com, © Justlight | Dreamstime.com, © Alexskopje | Dreamstime.com

r/GEICO via Reddit.com, © Justlight | Dreamstime.com, © Alexskopje | Dreamstime.com

I need your help: Add Komando.com as a preferred source on Google

I’ll bet your insurance company has sent this one your way: “Drive safely, get rewarded. Sign up for our smart driving program today!” You’ve got a squeaky clean driving record, so what’s the harm?

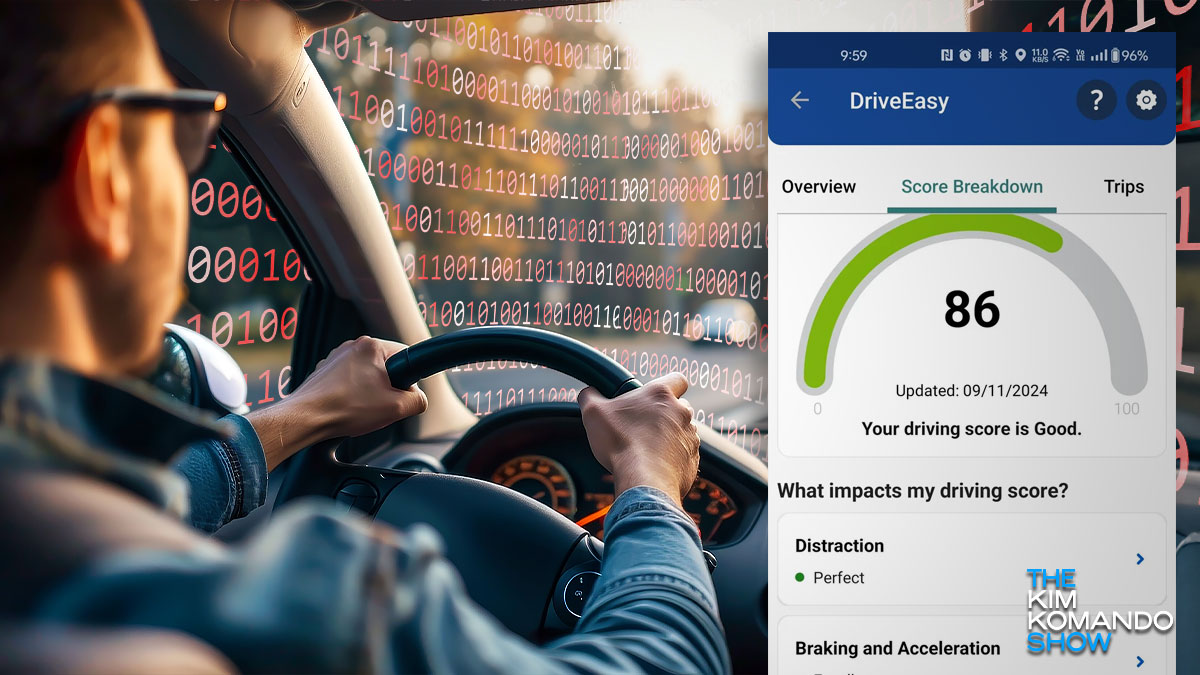

Smart driving programs track your driving habits and give you discounts for being a good driver. But there’s more to it than just saving a few bucks. Buckle up — I’ll break it down for you.

Know what’s being tracked

These programs monitor your driving habits using an app on your phone or a small gadget installed in your car. That data is combined with other factors, like your age, ZIP code and driving history, to calculate a score.

If the score is good enough, you might get a discount — think anywhere from 10% to 30% off your premium. Pretty sweet, right? But the discount comes with hidden costs.

They watch your every move

State Farm dings you if you go 8 miles per hour over the speed limit. So what happens if you floor it to avoid an accident?

GEICO and Allstate both tell you to avoid late-night driving since it’s the riskiest time for fatal crashes. But what if you work late or your kid has soccer practice that finishes after dark?

Ask your insurance company exactly what data they collect and how it’s used. Look for details on:

- Speed, braking and acceleration habits

- Late-night driving penalties

- Phone usage tracking

Maybe more importantly, what happens to your driving data after it’s collected? Does your insurance company share it with third parties or use it for marketing? Can it be sold or handed over in legal situations? Review those details before you agree to anything.

Your data could work against you

App-based programs track if you’re using your phone while driving. State Farm, Allstate, GEICO, Progressive and Travelers all monitor phone distractions. You should never text while driving, but it’s not as simple as that.

Say your phone screen turns on in your pocket or detects any movement. Boom, you’re marked for distracted driving. There are a few ways to avoid accidental “dings.”

- Keep your phone secured. Stick it in a compartment or use a phone mount. This is a solid option under $10.

- Turn off notifications or enable Do Not Disturb while driving.

You might pay more

Some companies, like GEICO and State Farm, may raise your rates if they flag your driving as “risky,” and Allstate could hike your premiums for bad habits they spot over time. The catch? They don’t spell out how each behavior impacts your rates.

Read the fine print: How long are you locked in? Ask if your data can still be used to raise rates later, even after you leave the program.

There are other ways to save

If handing over your driving data feels too invasive, consider a different way to trim your insurance bill:

- Bundle up. Combine your home or renters insurance and your auto insurance with the same company to save.

- Ask about options. Look for pay-per-mile plans if you don’t travel far. Defensive driving courses can shave 5% to 20% off your premium, too.

- Shop around. Compare rates annually to see if you’re still getting the best deal. Tools like Progressive’s AutoQuote Explorer and Policygenius cut out some of the legwork.

🚘 Did you hear about a new university program for used car salespeople? It’s a B.S. in Car‑deal‑ology. (Admit it, you laughed.)

Don’t get left tech-behind – Stay tech-ahead

Award-winning host Kim Komando is your secret weapon for navigating tech.

- National radio show: Find your local station or listen to the podcast.

- Daily newsletter: Join over 650,000 people who read The Current (free!).

- Watch: On Kim’s YouTube channel.

- Podcast: “Kim Komando Today” — Listen wherever you get podcasts.